Market Update: Exits & Liquidity

At our annual meeting, we shared a deep dive on exits and liquidity in today’s venture environment—highlighting the key data and trends shaping the path to returns. The bar to go public remains extremely high, there are more "creative" M&A deals happening, and a growing number of startups are stuck in “Zombieland”—with no clear path to exit.

Below is a recap of that presentation and corresponding graphs.

Exits and Liquidity Landscape

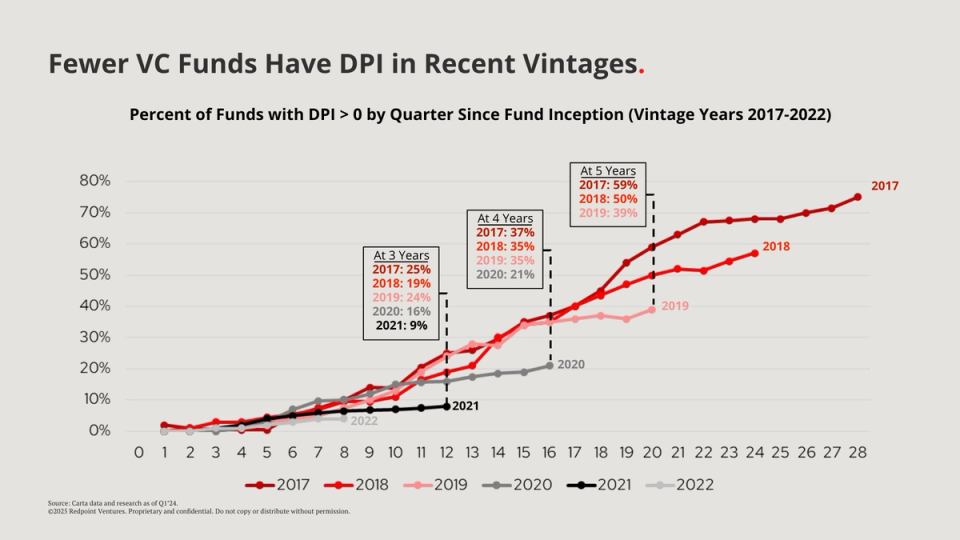

Carta published data last year that shows something we’ve all been aware of in venture the last few years. With a weaker IPO and exit environment, liquidity has been harder to come by, and recent venture vintages have struggled to produce DPI.

The percentage of recent vintages that have produced any DPI is at all time lows and well behind where older vintages (like 2017-2018) were 3 to 5 years after fund activation.

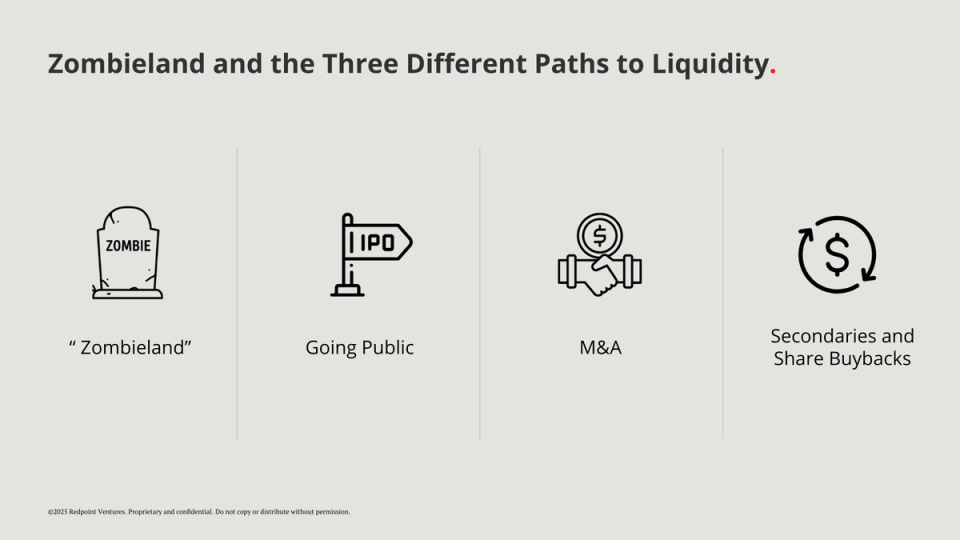

Startups are generally pursuing three main paths to liquidity—but beyond that, there’s a growing group of companies with uncertain outcomes, which we’re referring to as “Zombieland.”

Below is the data for companies that are stuck in “Zombieland.” Zombieland refers to a state of purgatory where it’s unclear how exits are going to be realized.

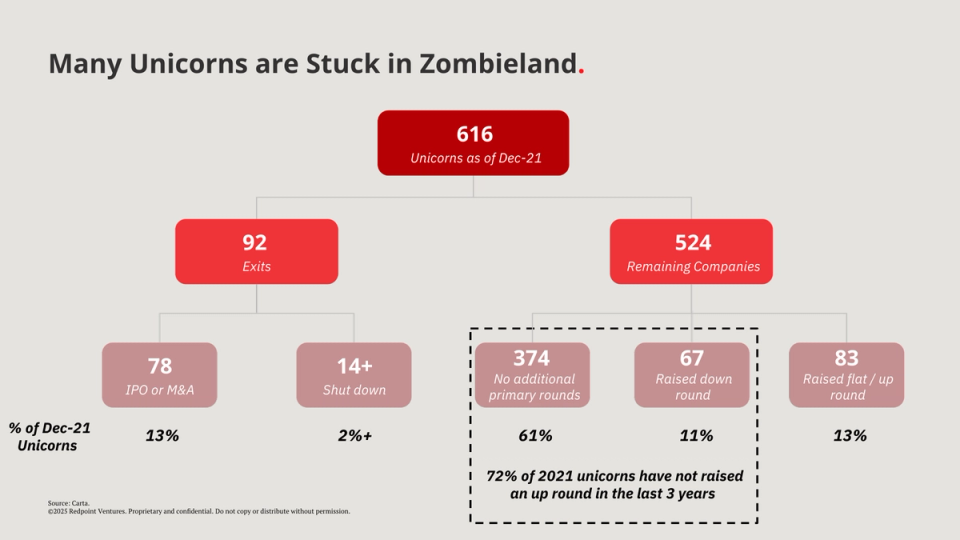

According to Carta data, there were 616 unicorns as of December 2021.

61% of those 2021 unicorns haven’t raised an additional primary round, and 11% have raised a down round.

There are obviously some larger companies that haven’t needed to raise additional capital, like some of the scaled businesses we mentioned earlier, but more likely than not, the vast majority of these companies aren’t trending towards an IPO and unfortunately don’t have a clear path to an exit.

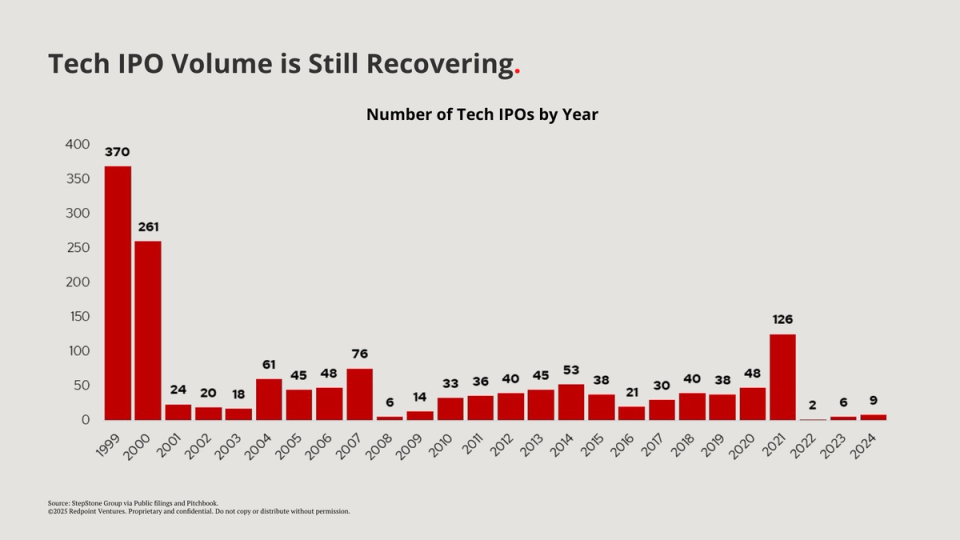

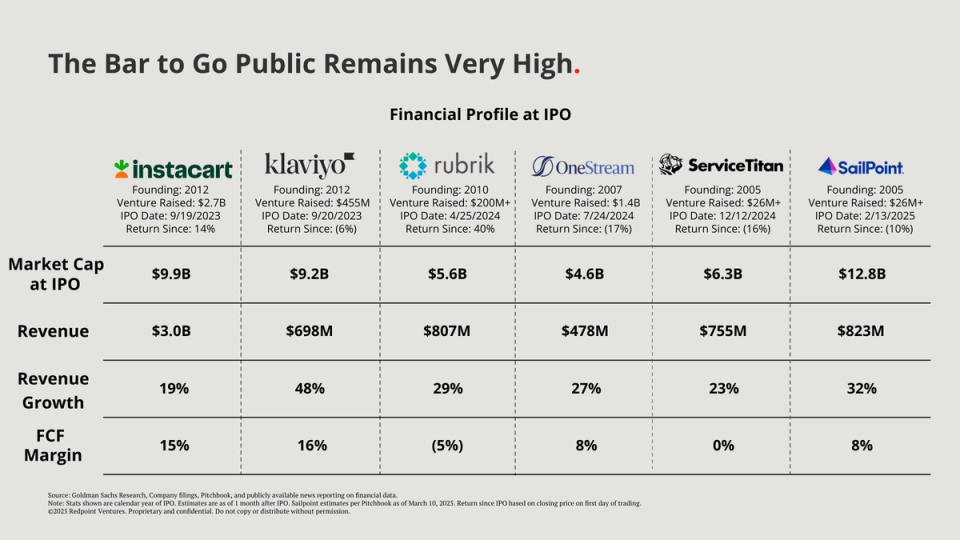

In looking at the traditional types of liquidity, Tech IPO volume peaked in 2021. The market has certainly started to recover, but still has a way to go before recovering to pre-COVID levels.

The companies that have made it to the public markets recently are all highly scaled—most were generating over $500M in revenue at IPO, growing 20%+ annually, and were either profitable or close to breakeven at worst.

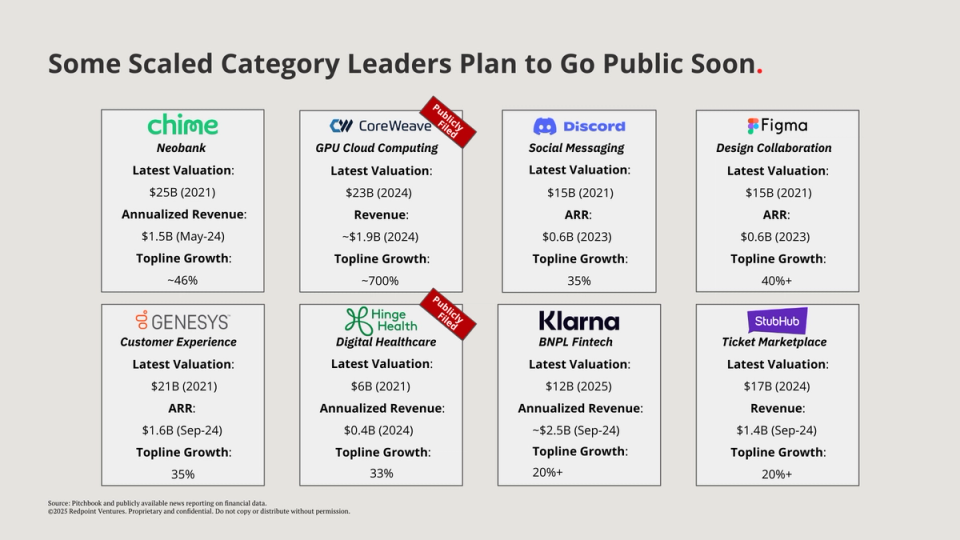

Below are some of the next tech companies slated to go public. These are all rumored to be going public sometime this year or have released their S-1.

The most notable thing: these are all scaled leaders with impressive growth.

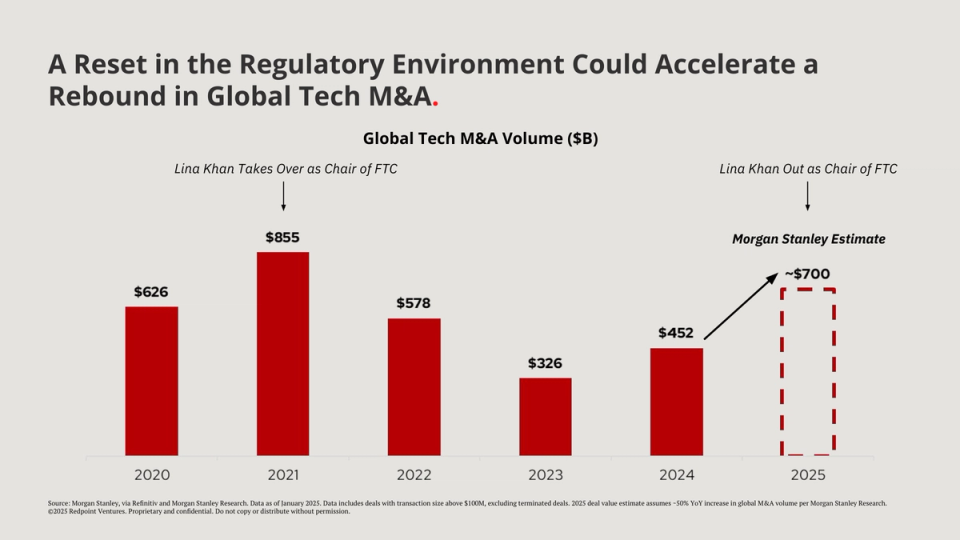

The next type of exit we have started to see more of is M&A. In tech, M&A deal volume peaked in 2021 at $855B. Since that point, we have seen a significant fall-off in M&A activity, which reached a low of $326B for global tech M&A in 2023.

After Lina Khan took over the FTC in 2021, there was significantly more regulatory oversight, and the EU became increasingly adversarial to acquisitions, which slowed down M&A deal volume. Adobe / Figma and NVIDIA / Arm are probably two of the most notable tech transactions that were called off due to extensive regulatory reviews.

Our own portfolio company Hashicorp had to suffer through this process with a 9-month long process that involved not just significant US regulatory scrutiny but also EU scrutiny.

Deal volume picked up again in 2024 as the market rebounded. With the new administration and leadership at the FTC, we expect that trend to continue. Morgan Stanley even estimates $700B of tech M&A volume in 2025, which would be the highest level since 2021.

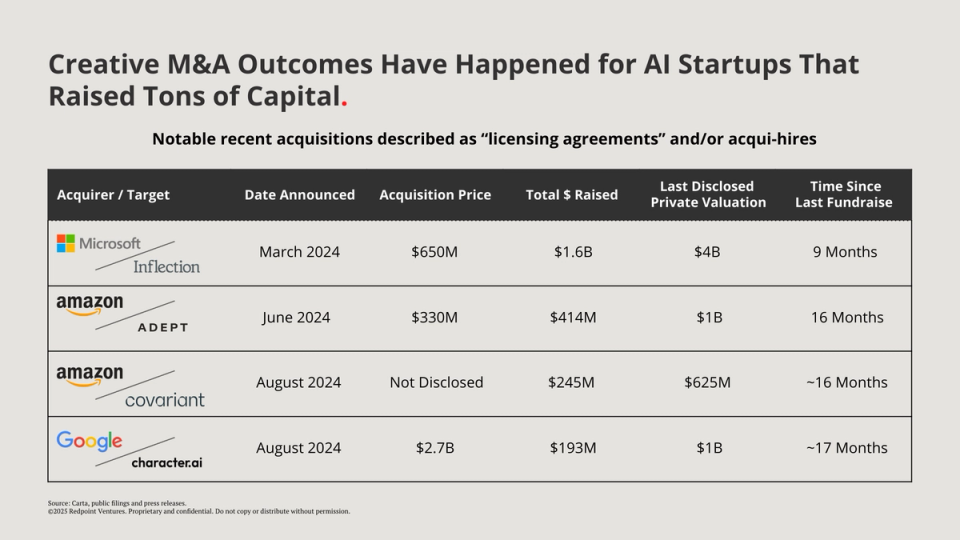

We’ve also seen some creative M&A deals happen in tech over the last year. The deals shown here all involved AI startups that had raised a ton of capital and hired really impressive technical teams.

The deals themselves were unusual - we saw big tech companies like Microsoft, Amazon, and Google effectively license the technology that startups had developed and hire away the stellar founding teams to lead AI R&D business units in their own organizations. Certainly a strange structure, but given the amount of AI startups that have raised tons of money in the last 2 years, it’s possible we see more exits like this.

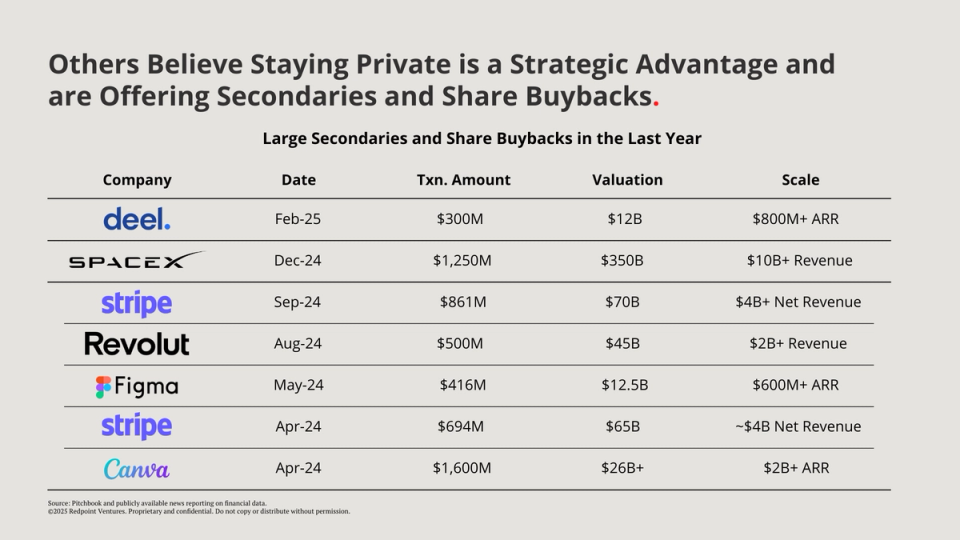

The final type of liquidity we’re seeing (which isn’t totally new but has become more scaled and more frequent lately) is sizable secondaries and share buybacks. These are large private tech leaders all of which are approaching or already surpassed $1B in revenue.

For some, if not all of these companies, staying private has actually become a strategic advantage. They’re able to continue investing heavily into R&D without public reporting requirements or wall street’s quarterly earnings reviews. This can be a real competitive advantage for these businesses especially since there is plenty of investor demand in the private markets to engage in secondaries to give employees and early investors the type of liquidity they would normally receive in an IPO.

This is an exit option that we’ve evaluated in the past and will continue to do so on a case-by-case basis going forward.

To conclude, private leaders have liquidity options, but there is a growing number of highly “valued” startups where the ultimate outcome remains unclear. Check out our public markets update and private markets update for more deep dives.